Have you ever wondered what happens if a remote contractor you’re working with gets hurt on the job? Take, for example, you hire an event marketing manager to cover an event in India, and they have an accident at the event. Are they covered by your standard business insurance? Should the contractor be covered under your policies?

Short answer: In most cases, no to both.

Most commercial policies you carry won’t extend to injuries sustained by independent contractors, and workers’ compensation typically applies to employees, not contractors. In many countries, insurers also deny claims when someone is misclassified. That’s why, as you hire across borders, you need to stay alert to local labour laws, insurance requirements, and liability rules.

One contractor injury in the wrong jurisdiction can trigger penalties that make you wish you had stuck to hiring within familiar territories. In the case of the scenario above, you may want to cancel the event and not showcase your brand in the first place.

The good news: this is preventable. Know the exposures, spell out who carries which insurance in your contract, collect proof of coverage, and confirm local requirements before the work starts. Put the right cover in place, and you can protect the person, your brand, and the event.

Why Workers' Compensation Usually Doesn’t Apply to Contractors

Workers’ compensation is a statutory, no-fault system that pays medical bills and a portion of wages when an employee is hurt or becomes ill because of work. You fund it through employer premiums; when a covered injury happens, the policy pays benefits.

For contractors, it is a different ball game. Most traditional workers’ compensation does not cover them, as they are considered self-employed and must arrange their insurance. But if you misclassify someone, by directing their hours, tools, and method of work, or making them economically dependent, authorities can treat them as your employee. Learn more about how to classify and pay remote contractors legally to avoid costly missteps.

Plenty of companies assume that they’re not legally obliged to cover contractors, so they don’t have to think about it—another wrong misconception. Even without a legal requirement, an uninsured contractor can still take legal action if injured during your project, especially if they’re economically dependent on you.

Get clear on who carries which insurance, put it in the contract, collect COIs, and confirm local requirements before work starts. Do that, and you protect the person, your budget, and your brand.

Insurance Options Every Remote Contractor Should Consider

Now, if you’re working with contractors, you should have options. There are quite a number of them, and you should pick based on your risk profile, knowing that there are multiple solutions available to you.

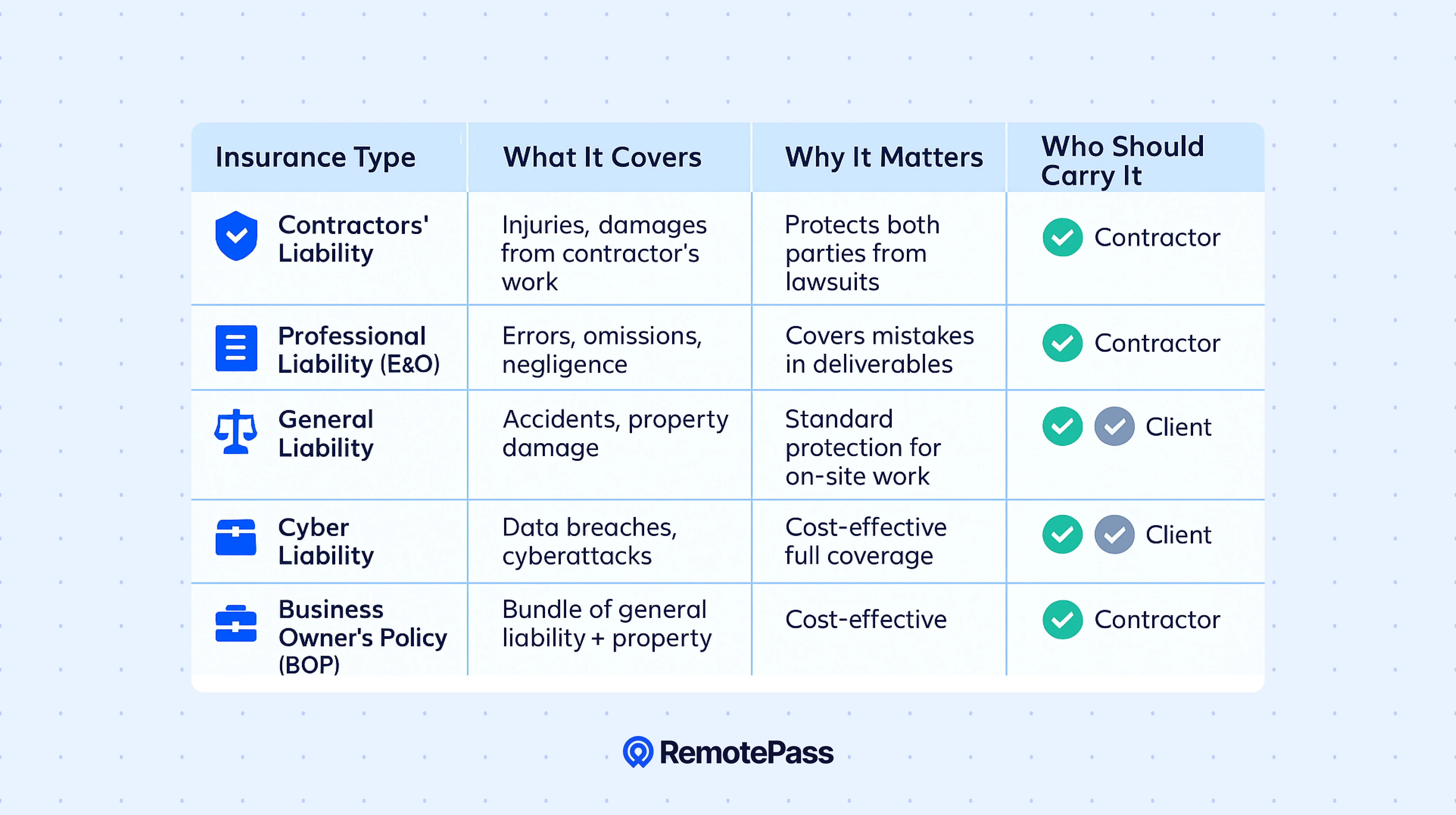

Specialised Contractors' Liability Insurance

What it covers: This coverage takes care of injuries to people or damage to property caused by the contractor while working.

Why it matters: Remote contractors may travel for work, handle client equipment, or work in shared spaces. If a videographer drops a camera on someone’s foot at a shoot or a field consultant damages a client’s equipment, this policy keeps the legal and financial fallout manageable.

Professional Liability (E&O) Insurance

What it covers: This insurance option covers situations where a contractor made a mistake, was negligent, missed deadlines, or delivered subpar work that caused financial loss to a client or partner. For example, if your developer deletes a client’s database, this option comes into place.

Why it matters: This coverage gives you breathing room when things go sideways and is especially important for knowledge-based roles like software developers, designers, marketers, or consultants. Without E&O coverage, you or your contractor might be footing that bill.

General Liability Insurance

What it covers: As the name implies, this plan covers more general and everyday risks. This could include a situation where there’s a home flooding at the contractor’s home office, damaging a laptop or a work device.

Why it matters: Think of it as the safety net for things that aren’t directly tied to delivering work but can still happen during the job. It’s often the first layer of defence for minor but expensive mishaps.

Cyber Liability Insurance

What it covers: Remote work relies on laptops, cloud platforms and home WiFi networks, and these are more vulnerable than secured office servers. Contractors could deal with data breaches, ransomware attacks, phishing scams, and other cyber incidents. This coverage can include legal fees, customer notification costs, data recovery, and even PR damage control.

Why it matters: If a contractor accidentally exposes sensitive customer data, the financial and reputational damage can be enormous. In 2025, this coverage is no longer optional for digital-first teams. Ensure that the policy covers both first-party losses (your data) and third-party claims (customer lawsuits).

Business Owner's Policy (BOP)

What it covers: For contractors who run their small businesses, a Business Owner's Policy (BOP) is a cost-effective package combining general liability, property insurance, and business interruption. This comprehensive coverage can save you money and time by bundling multiple protections into one policy.

Why it matters: A BOP can simplify protection by covering several risk areas at once, without juggling multiple standalone policies.

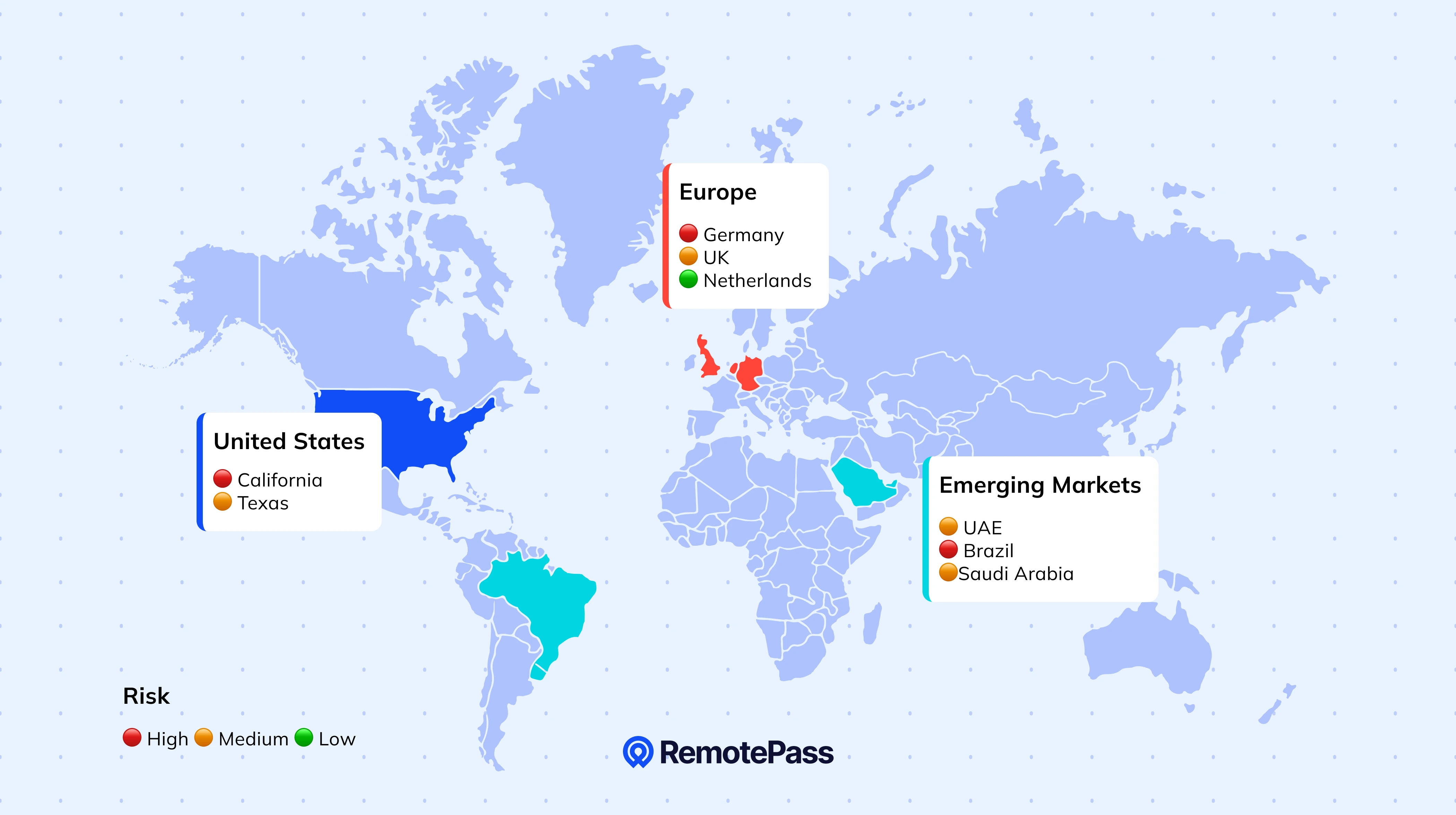

How Jurisdictional Laws Affect Contractor Coverage

When you hire remote contractors across borders, the hard part isn’t just picking the proper insurance; it’s that rules change depending on country, state/province, industry, and even how a local regulator interprets the term ‘contractor’. That variability is the root cause of most surprises: misclassification fines, unexpected payroll liabilities, or a local regulator deciding you owe back benefits.

Governments use different tests to decide who’s an employee vs a contractor, and these changes vary in regions.

United States

With 50 different states, the US has wildly different interpretations of contractor status.

- In California, the ABC test under AB5 is the strictest in the country. This test requires that contractors must pass all three parts, or they’re considered employees, triggering full workers’ comp requirements and, for many companies, six-figure back-premium bills.

- In Texas, there’s more flexibility with contractor relationships, but misclassification still leads to heavy penalties, including back wages, unpaid taxes, and workers’ comp premiums you thought didn’t apply.

Europe

European countries have some of the world’s strongest worker protection laws — and during COVID, many doubled down. Several nations used the pandemic as a springboard to tighten contractor protections and close loopholes they felt companies were exploiting.

- In Germany, the default assumption is that most working relationships are employment unless you can prove otherwise. If your contractor arrangement looks like a long-term, exclusive, or fully integrated role, it can trigger automatic employee status and backdated obligations.

- In the UK, the IR35 rules determine whether your contractor should be treated as an employee for tax and insurance purposes. Post-COVID, HMRC has been even more proactive in auditing arrangements, especially in remote work setups where roles can blur.

- Up in the Netherlands, the DBA law was designed to make working with contractors easier, but easier doesn’t mean hands-off. You still need clear contractual boundaries, proper insurance documentation, and proof that the contractor runs an independent business.

Emerging Markets

Emerging markets may have the fastest-growing contractor markets, but they’re also the most unpredictable when it comes to regulatory changes.

- Countries like the UAE and Saudi Arabia are rapidly developing contractor frameworks as they diversify their economies. The repercussion? What’s legal today might require different insurance coverage tomorrow.

- In Brazil, however, most contractor relationships are employment by default, requiring extensive documentation to maintain independent status. Miss the requirements, and you're looking at hefty labour court settlements.

Here's what keeps everyone awake at night: these rules don't stay put. Labour laws evolve, court decisions shift precedents, and tax authorities update their guidance regularly. A compliant contractor relationship in January might be a liability by December.

Monitoring regulatory changes across multiple jurisdictions means subscribing to legal updates in different languages and staying current on tax authority guidance. Most companies either miss critical changes or spend a fortune on legal fees trying to keep up. This is precisely where RemotePass becomes the necessary tool in your arsenal, especially through our Contractor of Record (CoR) model designed to simplify global hiring and insurance compliance.

Instead of playing regulatory roulette, our system monitors 150+ countries and automatically updates your compliance requirements. When Germany tweaks its contractor rules or Texas changes its classification criteria, you know immediately and not when you're facing penalties. It’s like having a local legal expert in every jurisdiction without the budget.

Best Practices to Reduce Legal & Financial Risk

The best companies think ahead of the curve by building an agile workforce plan and protecting themselves early without losing sleep or breaking the bank.

1. Conduct Risk Assessments Before Hiring

Not all contractor relationships carry the same risk. A graphic designer creating social media posts carries different liability exposure than a DevOps engineer with access to your production systems.

Risk factors to evaluate:

- Access level: What systems, data, and facilities will the contractor access?

- Project value: Higher-stakes projects warrant more comprehensive coverage

- Duration: Long-term relationships increase classification risks

- Location: Some jurisdictions have stricter requirements than others

- Work type: Physical vs. digital work carries different injury risks

2. Verify Insurance Coverage and Contract Eligibility

Don't just ask for proof of insurance. Verify it also. Request certificates of insurance directly from the contractor and say no to screenshots, as those could easily be fabricated.

Insurance verification checklist:

- Ensure that coverage amounts meet your project requirements

- Ensure that the policy is current and won't expire during the project

- Ensure that your company is listed as an additional insured (when appropriate)

- Ensure that the coverage includes the type of work being performed

- Set calendar reminders for policy renewal dates. Expired coverage is the same as no coverage.

3. Use Contracts to Clarify Responsibilities

Your contractor agreement should explicitly address insurance requirements and responsibilities.

Key Clauses To Place:

- Minimum coverage requirements by insurance type

- Additional insured status for your company, where appropriate

- Indemnification clauses that shift certain liabilities to the contractor

- Notice requirements for claims or coverage changes

- Right to verify coverage throughout the project

Pro tip: Standard contract templates often miss jurisdiction-specific requirements. RemotePass' global payroll platform includes a contract generation system that creates locally-compliant agreements that protect your interests while meeting local legal standards.

4. Stay Updated on Regulatory Changes

Compliance isn't a one-and-done task. Labour laws, insurance requirements, and classification tests evolve constantly. Set up systems to monitor changes in your key markets.

Monitoring strategies:

- Get started with platforms like RemotePass that track regulatory changes automatically

- Subscribe to legal updates from employment law firms in key jurisdictions

- Set Google Alerts for regulatory changes in your contractor locations

5. Leverage Technology for Compliance Management

Managing insurance compliance manually across multiple contractors and jurisdictions is a recipe for costly errors. Modern platforms like RemotePass can automate much of this complexity, giving you time to refocus on other projects and tools to stay compliant across multiple countries.

How RemotePass Supports Your Insurance and Compliance Needs

You could keep spreadsheets, track laws in multiple time zones, and negotiate policies one-by-one, or you could let RemotePass handle it. With us at the forefront of your insurance and compliance efforts, you get:

- Integrated payroll and compliance: One platform to pay, insure, and manage contractors anywhere.

- Local law coverage: Built-in compliance tracking for over 180 countries.

- Insurance partnerships: Direct access to vetted global providers like SafetyWing for workers’ comp-style and health coverage.

- Automated documentation: Proof of coverage, compliance reports, and contract terms all stored in one place.

- Open APIs: RemotePass API integration ensures seamless syncing of payroll, compliance, and insurance data across your HR tools.

The result? You’re able to scale your team with no headaches. Ready to turn contractor insurance from a mystery into a competitive advantage?

Book a demo or get started for free to experience seamless compliance in over 150 countries.

.svg)

.svg)