When HR leaders ask “How do you actually pay international employees?” on community forums, answers range from “just use Wise or PayPal” to “you almost certainly need an Employer of Record (EOR).”

That mix of half-solutions and guesswork reflects a real problem: many teams are mixing up simple money transfer with legal payroll compliance, and that’s exactly the gap this guide closes.

You’ll learn how to pay international employees legally, efficiently, and without triggering compliance risks across each model: legal entity, EOR, and contractors. Let’s start at the root: your hiring method.

Payroll Starts with Your Hiring Method

The way you hire a worker (whether as an employee or independent contractor) defines their classification. And that classification decides how you pay them, which taxes apply, and what legal responsibilities you take on.

Get it wrong, and you’re stepping into a compliance trap that could cost you penalties and (if regulators get serious) an operational freeze.

So how do you get classification right?

Start with the basics. Here's a simple way to think about it:

- Employees follow your lead, earn a set salary, and work inside your workflows

- Contractors control how they work, juggle multiple clients, and handle their own taxes

Still unsure? Run this quick test:

- Do you set their daily schedule or work methods?

- Do they work exclusively for you?

- Do you provide tools or benefits typical of employees?

If the answer is “yes” to most, you probably have an employee, and that changes your payroll obligations.

If you're unsure, get legal advice or use an Employer of Record (EOR) to stay compliant. Whatever the scenario, keep documentation and review status regularly to stay compliant.

For a deeper walkthrough of how to decide whether someone is an employee, contractor, or something in between, see our guide on

hiring international employees

.

Once you’ve classified someone, here’s how payroll works for each hiring method.

How to Pay International Employees Based on Your Hiring Method

How to pay international employees depends entirely on your hiring method. Each setup comes with different compliance requirements and changes what you’re responsible for, from payments to reporting.

Let’s break down what those differences look like in practice once someone’s hired, and it’s payday.

How to Pay International Employees Through Your Own Legal Entity

One way to solve how to pay international employees is to set up your own legal entity in the hire’s country.

When your company has a legal entity, you’re the legal employer and responsible for full compliance.

This gives you control over payroll, but also makes you accountable for local taxes, contributions, reporting, and labor laws.

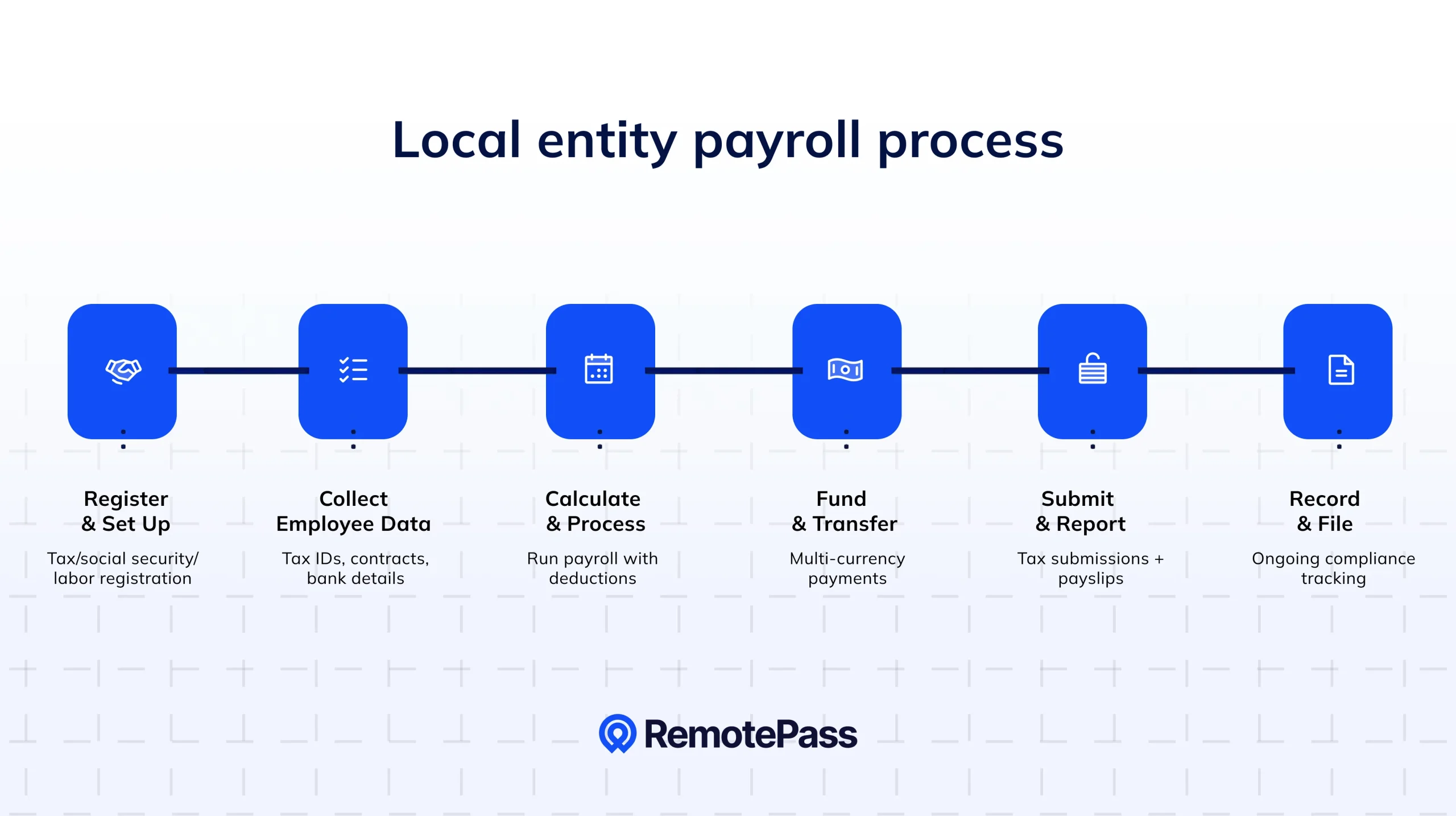

How payment works under this setup (step-by-step)

You’ve got a local entity, now payroll’s on your desk. Here’s how it plays out.

- Register as an Employer and Gather Local Requirements: You’ll need to register with tax, social security, and labor authorities. This usually requires a local business number, supporting documents, and a bank account in local currency. Registration is what makes payroll legal, not optional.

- Collect and Verify Employee Info: You’ll gather accurate tax IDs, contract terms, bank details, and benefit elections. Mistakes here cause miscalculations and compliance issues down the line.

- Run Payroll Accounting and Deductions: Using a payroll calendar, you (or a vendor) calculate gross pay, apply deductions and contributions, and process the run based on local rules.

- Fund and Reconcile Payments Across Currencies: You’ll manage FX rates, cut-off times, and multi-currency payments to ensure funds land on time. Delays erode employee trust and trigger fines.

- Submit to Authorities and Generate Payslips: Once payroll is complete, submit taxes and contributions to local authorities and issue payslips that meet legal standards.

- Keep Records and File Reports: You’ll need to track reporting windows, file ongoing reports, and store records for audits. Missed filings trigger fines and tax authority attention fast.

Without careful tracking of payroll timing and reporting windows, it’s easy to miss deadlines. And those misses compound quickly in tax authority risk and financial exposure.

Tools you can use to process payroll

While the steps above are the what, the how depends on your scale and setup.

Here are some practical solutions companies use when handling entity-based payroll, each with tradeoffs worth knowing:

- Using local payroll providers: Reliable in one country, but hard to scale across multiple markets

- Using global payroll platforms: Enables multi-country payroll if you already have local entities

- Building internal systems: Offers full control but requires ongoing legal upkeep

- Automating payroll workflows: Reduces manual errors and keeps your tax logic up to date

Running payroll through your own entity gives you control. Without local compliance, though, it doesn’t count as legal payroll.

But what if you don’t have a legal entity in the country where your hire lives? That’s where an EOR steps in.

Just published

The 2025 Remote Hiring Report

What 35k contracts reveal about the future of global teams.

How to Pay International Employees Through an Employer of Record (EOR)

An Employer of Record (EOR) is a third-party service that legally employs workers on your behalf in countries where you’re not set up. They handle employment contracts, payroll, taxes, benefits, and compliance, while you manage daily work.

For companies trying to figure out how to pay international employees without setting up local entities, an EOR is the compliant shortcut. You get to start quickly and stay compliant with local employment laws.

One often-overlooked benefit: EORs help reduce permanent establishment (PE) risk.

Because the EOR is the legal employer, there’s a layer between your business and local tax authorities. This can lower your exposure to corporate tax risk in that country.

Case in point: Chaos, a 3D visualization company, needed to hire full-time specialists in Vietnam, India, and Mexico. But they didn’t want to set up legal entities in each country, which could trigger PE risk and compliance obligations.

By working with RemotePass, they hired 15 employees across nine countries and saved $135,000 in setup costs. RemotePass became the legal employer, letting Chaos scale quickly without taking on the burden of compliance themselves.

But, PE risk isn’t eliminated entirely. If your hires are generating significant revenue or acting as agents under local law, tax authorities may still see your company as having a taxable presence, even with an EOR.

How payment works under this setup (step-by-step)

With an EOR, the complexity stays off your plate. Here’s how it works behind the scenes.

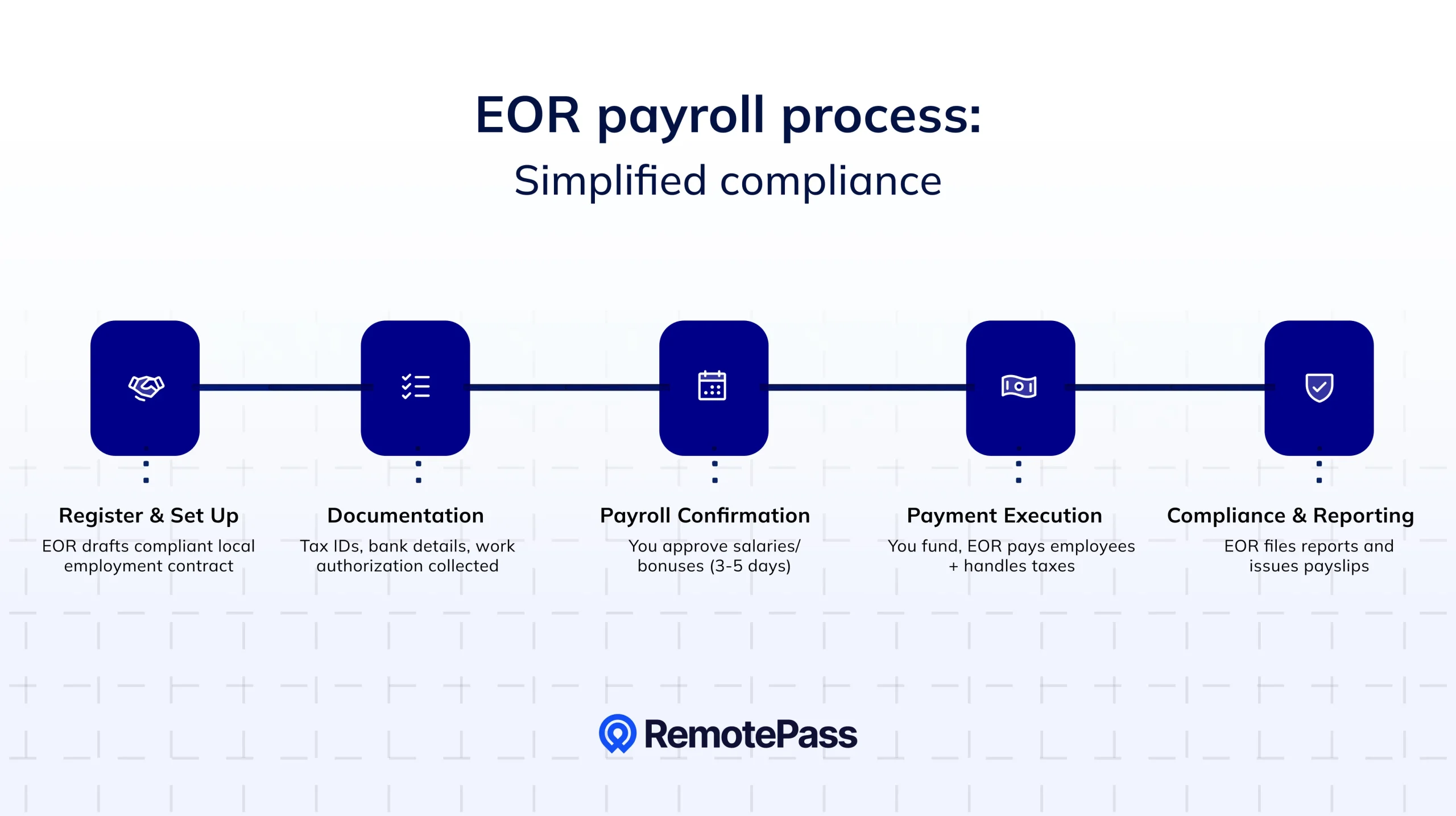

- Local Contract Setup: Once you choose a candidate, the EOR drafts and signs a compliant employment contract under local law, including required benefits and termination terms.

- Documentation and Approvals: The EOR gathers tax IDs, bank details, and work authorization documents, and ensures all parties have signed. This sets payroll in motion.

- Payroll Confirmation: Before each pay run, the EOR confirms salaries, bonuses, and deductions with you. This typically takes three to five business days, faster than most entity-based payroll cycles.

- Payment Execution: You fund the payroll (often in one transfer), and the EOR pays employees, withholds taxes, and remits contributions locally.

- Compliance Filings and Reporting: The EOR files required reports and issues payslips that meet local legal standards; no action needed from your side.

The EOR handles operations, but you still need to align on timing and documentation so your finance team can plan ahead and avoid payroll delays.

What You’re Responsible For vs What the EOR Handles

One of the biggest mistakes companies make with an EOR is not knowing where their responsibility ends. That gap leaves your team exposed to audits and internal confusion.

What the EOR handles:

- Legal employment contracts and compliance with local labour law

- Payroll processing, tax withholding, and statutory contributions

- Benefits and statutory reporting

- Filings with local authorities

You’re still responsible for:

- Setting pay and compensation details

- Managing the employee’s daily work and performance

- Watching for PE risk, especially if the role touches significant revenue

The EOR handles paperwork and compliance. You still own the relationship and the risk if it crosses legal boundaries.

Want to see how RemotePass handles this?

Check out our breakdown of

what an EOR can and can’t do

.

An EOR helps you scale fast and stay compliant, but you still need to understand who owns what. That’s how you avoid missteps and keep hiring on track.

But what if you want to hire a contractor?

How to Pay International Contractors

Hiring a contractor means paying a self-employed business, not putting someone on payroll. That gives you flexibility, but only if the role meets local contractor rules.

How payment works under this setup (step-by-step)

Paying contractors looks simple. But here’s what it really takes to keep it compliant:

- Agree on Scope and Contract Terms: Sign a contract that defines deliverables, deadlines, fees, and IP ownership. This is the first thing regulators check, so the language should reflect contractor autonomy.

- Collect Tax Documentation: Collect the required local tax forms or proof of tax residency (whatever applies in the contractor’s country). You don’t always need to submit them to authorities, but you do need to keep them on file as proof you collected the right documentation.

- Choose Your Payment Method

Your method changes how fast money moves and what it costs to get it there:- Bank transfers: stable but slow

- Platforms like Wise, PayPal, or Payoneer: faster and cheaper

- Contractor wallets: contractors choose how and in what currency they get paid

- Collect Invoices: A contractor must invoice you for each payment you make. Before payment, you need to check the invoice is compliant and matches the completed work.

- Process the Payment: Once the invoice is approved, send the funds. Contractors pay their own taxes; there are no withholdings on your side.

- Record and Store Documentation: Save contracts, invoices, payment records, and tax forms. You’ll need airtight records to defend against a misclassification challenge.

Choose your payout method wisely, but remember, speed means nothing if the legal foundation isn’t solid.

What to Check Before Paying a Contractor

There’s more to paying a contractor than hitting “send” on a transfer. Before any money moves, confirm the engagement is compliant:

- Classification Fit: Confirm the contractor has true autonomy.

- Country-Specific Tax and Registration Quirks: Some countries require tax forms, VAT filings, or local contractor registration. Missing these triggers fines and unexpected tax obligations.

- Proof of Autonomy and Payment Trail: Keep contracts, tax forms, and work records before paying, as your defense if the classification is ever challenged.

- IP Rights Secured: Make sure your contract locks down IP ownership before work begins.

Paying international contractors gives you control, but also puts the compliance burden on your team.

A Contractor of Record (CoR) offers a simpler path: you keep the flexibility of contractor engagements, but offload the risk and admin.

A CoR manages the entire contractor relationship on your behalf:

- Drafting compliant contracts

- Handling tax documentation and invoicing

- Processing payments

- Maintaining a local audit trail

A CoR doesn’t employ the worker, but it preserves their contractor status while helping you stay compliant with local laws.

Use a CoR when:

- You’re hiring contractors in countries with complex or evolving contractor rules

- Your internal team cannot reliably maintain contractor compliance

- You want to reduce contractor misclassification risk

- You want to scale global contractor hiring without switching to an EOR

- Consolidating into one invoice in your Enterprise Resource Planning (ERP) system instead of onboarding each contractor separately and receiving multiple invoices

If you're scaling global contractors and want operational peace of mind, a CoR can save you a lot of headaches.

Each model comes with its own mix of rules and flexibility. Here’s how they stack up side by side.

How to Pay International Employees: Entity vs. EOR vs. Contractors Compared

Here’s how responsibilities, compliance risk, and payment setup differ across each model, so you can choose the right fit and know what to do next.

| Aspect | Entity Payroll | EOR Payroll | Contractor Payroll |

|---|---|---|---|

| Who employs them? | You | The EOR | They’re self-employed |

| Who manages compliance? | You handle all taxes, filings, and benefits | EOR handles local compliance and filings | Contractor manages their own taxes |

| Speed to hire | Slow; entity setup takes months | Fast; onboard in days or weeks | Fast; sign a contract and start immediately |

| Your role in payroll | You manage everything: setup, pay runs, taxes | You approve pay; EOR processes payroll | You pay invoices; the contractor handles taxes |

| Misclassification risk | Low (if setup and classification are correct) | Low (depends on role structure) | Varies per country (this can become an issue if you have an entity where the contractor is based) |

| Best for | Long-term presence in a country | Quick expansion without legal setup | Short gigs and flexible projects |

In short:

- Entity Payroll = full control + full responsibility. Best for long-term growth in a market.

- EOR Payroll = fast + compliant. Best for quick hires where you don’t want to set up an entity.

- Contractor Payroll = flexible + simple. Best for project work (if the role really fits a contractor model).

Even with the right model in place, many teams still slip up. Here’s where international payroll gets tricky, and how to stay ahead of it.

Common Pitfalls with Paying International Employees (and How to Avoid Them)

Payroll is a legal process with country-specific rules. Without a clear process, it’s easy to misclassify roles or trigger penalties. Here are the most common mistakes teams make, and how to avoid them:

Misclassifying Employees as Contractors

Misclassification ranks among the costliest global payroll errors.

Regulators ignore what your contract says. They inspect how the work happens: who controls the schedule, whether the worker relies on your company for income, and how integrated they are in your daily operations.

The rules vary by country, but if your contractor follows your direction and keeps fixed hours, they may qualify as an employee, no matter what the contract calls them.

That matters because employers must pay employees through payroll, with taxes withheld and employer contributions added directly. Contractors, on the other hand, are typically paid in full without withholding and handle their own taxes.

Mistakes here trigger fines, back taxes, unpaid benefits, and legal liabilities. In Europe and beyond, enforcement ramps up fast, with audits and penalties hitting without warning.

How to avoid it:

- Use indicators like control and autonomy, not just job titles

- Reassess roles as they evolve. A short gig can morph into a full-time relationship

- Keep records that show how work is done, not just what’s on your contract

Getting classification wrong drags in finance, HR, and legal, and leaves everyone exposed. Solve this before the first payment goes out.

Paying Without Proper Local Registration

Payroll is a regulated process that requires tax and social security registration in the employee’s country of residence. Every country has its own payroll laws and compliance standards.

Skip this step, and you can face retroactive contributions and multi-year audits. In many countries, unregistered payroll is a violation on its own, even if you paid the right amount.

How to avoid it:

- Confirm employer registration is complete before you process payroll (including tax and social security accounts)

- Use a checklist for each country with filing deadlines and required IDs

- Track payroll calendars globally to avoid clashes in timing or cash flow

No registration means no legal payroll, and a high chance of penalties if audited.

Missing Tax and Reporting Deadlines

Global payroll means staying aligned with each country’s tax and filing deadlines, not just processing payments.

Each country has its own deadlines for tax remittances and compliance filings. Miss them, and you could face fines or even operational suspension. In some markets, one missed report can trigger audits across multiple years.

Take Brazil and Germany, for example:

Brazil requires tax and social security payments within days of payroll. Germany expects detailed monthly filings by strict deadlines. If you’re late in one region, overlapping calendars can cause penalties to pile up quickly.

How to avoid it:

- Build a payroll calendar that maps every country’s reporting dates

- Align it with your internal pay cycles, especially across time zones

- Use centralized tools that flag obligations and send automated reminders.

This is exactly where many teams move from spreadsheets to platforms like RemotePass EOR, where calendars and compliance alerts are built into the workflow.

Global payroll isn’t a set-it-and-forget-it system. It’s a recurring compliance event, and one missed step can trigger a chain reaction.

Underestimating the True Cost of International Payroll

International payroll costs go far beyond salary and taxes. Most teams miss the hidden costs of compliance and currency.

Statutory contributions and benefits often add 15-30% on top of base salary, including social security, pensions, health funds, and paid leave. These vary by country and must be factored into payroll from day one.

If you’re not tracking legal upkeep and multi-currency workflows, compliance overhead can quietly snowball into a serious cost.

Other common cost drivers:

- Late compliance penalties (often retroactive)

- FX fees and exchange rate spreads

- Reserve requirements in some countries

How to budget properly:

- Start with gross salary

- Add mandatory contributions and benefits

- Factor in legal, admin, and FX costs

- Build a buffer for timing gaps and late fees

We’ve seen 20-30% budget overruns when teams skipped these extras, often before the second payroll run. Here’s how RemotePass helps cut those costs before they spiral.

If you don’t price in the full picture, your hiring budget can quickly turn into a liability.

The Global Payroll Playbook: Make the Right Move at the Right Time

Paying people internationally means knowing who you're hiring, what you’re responsible for, and how your model affects the timeline.

When you tie payroll to classification and build workflows around that model, you eliminate ambiguity and reduce risk..

Sounds simple. But doing it right, on time, every time, is where teams can slip up. That’s exactly where RemotePass comes in.

RemotePass handles payroll and compliance in 150+ countries, using the right model for each hire. Your international team gets paid on time, within local law, and without compliance stress.

Book a demo and see what reliable, compliant global payroll looks like in action.

FAQs on How to Pay International Employees

1. How does international payroll work?

International payroll means collecting employee info (tax IDs, bank details, contract terms), calculating gross-to-net pay with local taxes and deductions, sending payments in the correct currency, and filing with local authorities.

The process changes depending on whether you use your own entity, an EOR, or contractors, because compliance rules vary across models.

2. What are the risks of paying international employees incorrectly?

The big ones: permanent establishment, misclassification, unpaid taxes, data privacy issues, and employee disputes.

Mistakes here can cost six to seven figures and trigger audits that slow down hiring.

3. How long does it take to set up international payroll?

It depends:

- Contractors can start immediately with a signed agreement

- EORs can onboard employees in one to two weeks

- Setting up your own entity takes three to six months

If you already have entities, setting up a global payroll platform takes two to three months. First payroll runs usually add two to three extra weeks for data collection and setup.